Highlights

- While only a slight uptick in average close price overall, attached homes set an all-time high with an average of just over $504k.

- Available inventory jumped nearly 66% (and is up 94% over last year), boosting supply over 1 month (to 1.12) for the first time in 2 years.

- Despite higher interest rates, more supply will mean better opportunities for buyers with homes on the market longer leading to lower sales prices.

Inside the Numbers

-

5,090 HOMES CLOSED

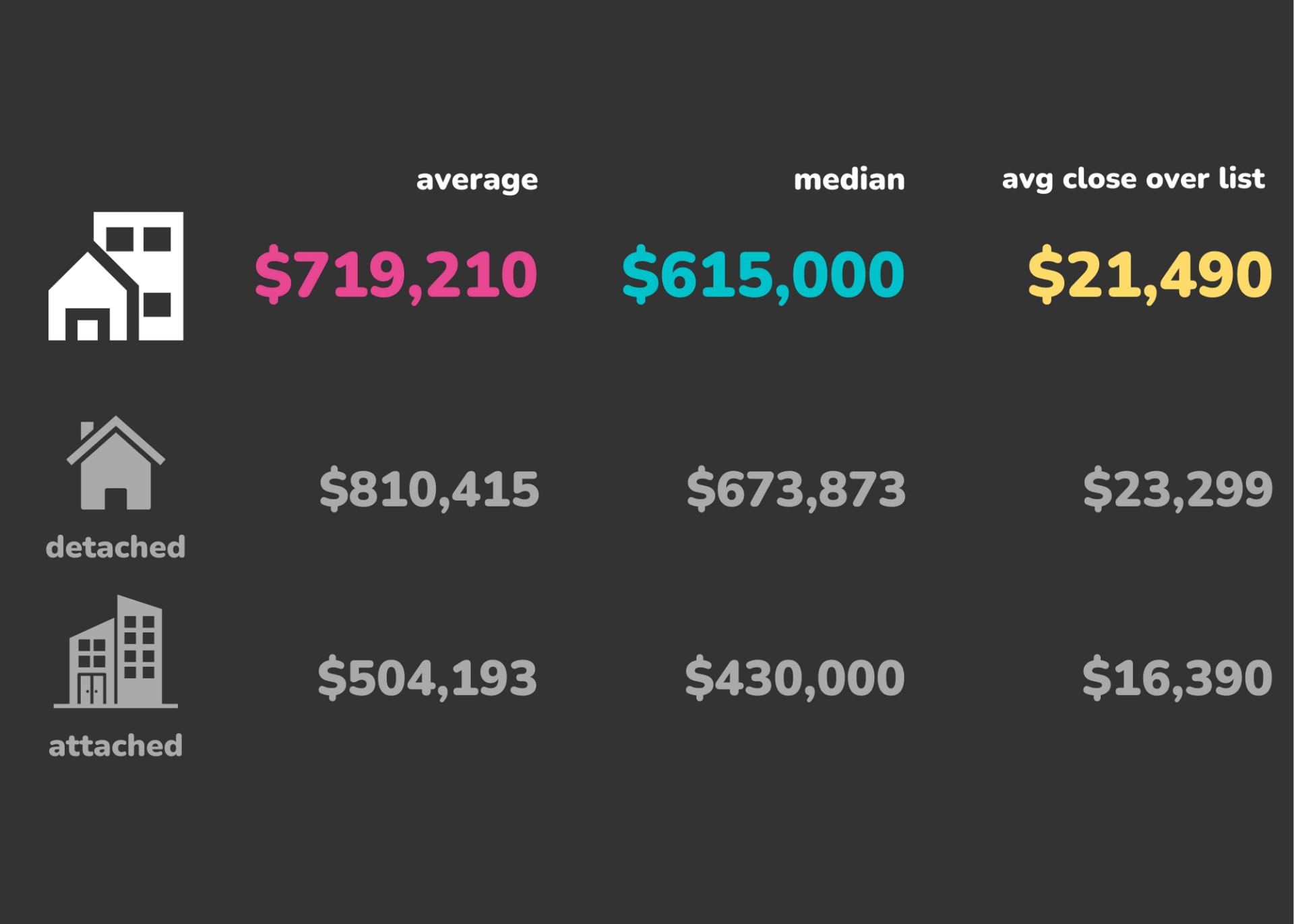

Sales Price Breakdown

Average sales prices are up slightly from May and down from April, while buyers are paying $26k less over the list price than 2 months prior.

-

7,717 NEW LISTINGS

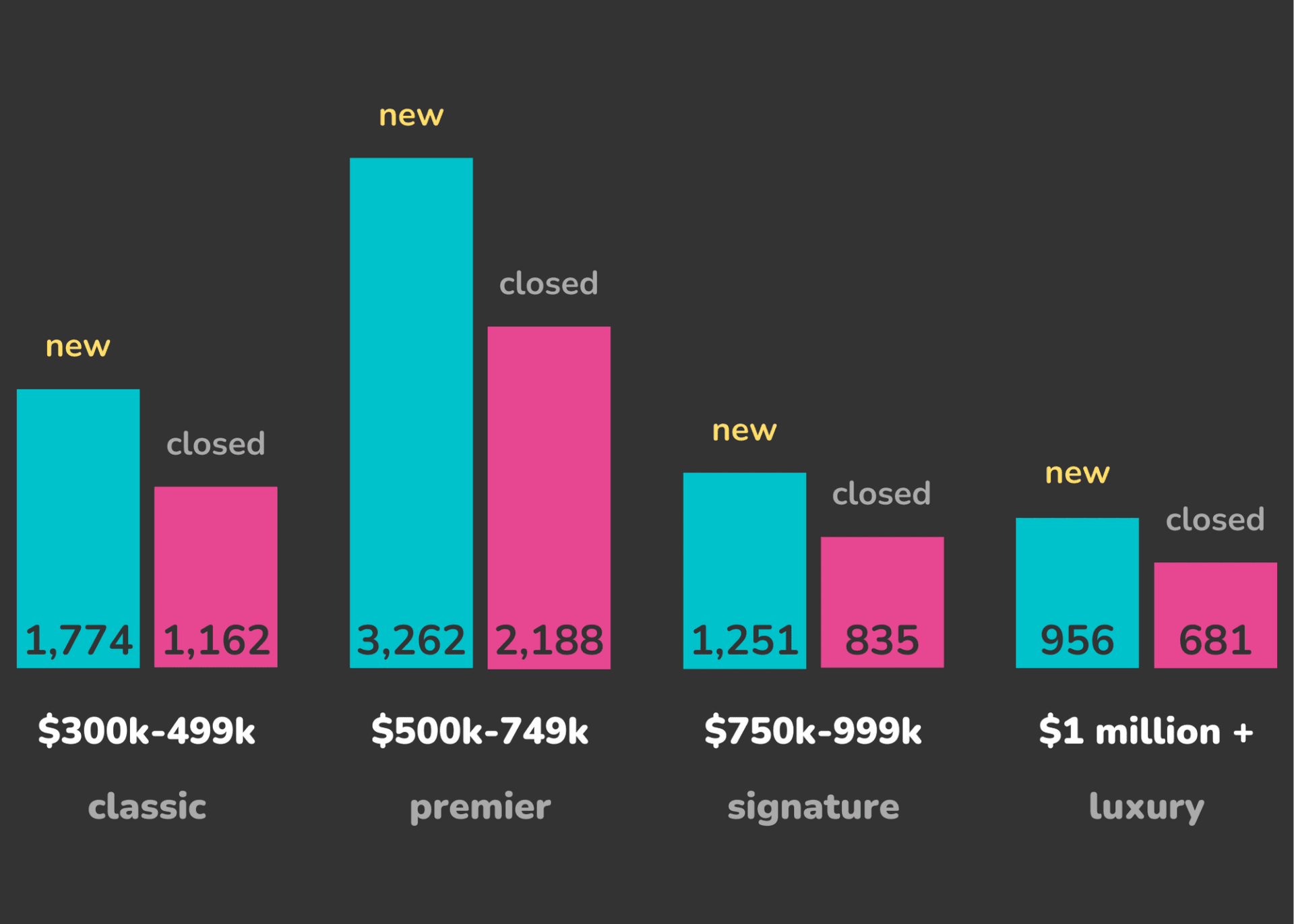

New Listings V. Closed Sales

Part of the inventory surge can be attributed to a wider gap between new listings (up 13%) and closed sales (down 12%) across all segments.

-

4,943 HOMES UNDER CONTRACT

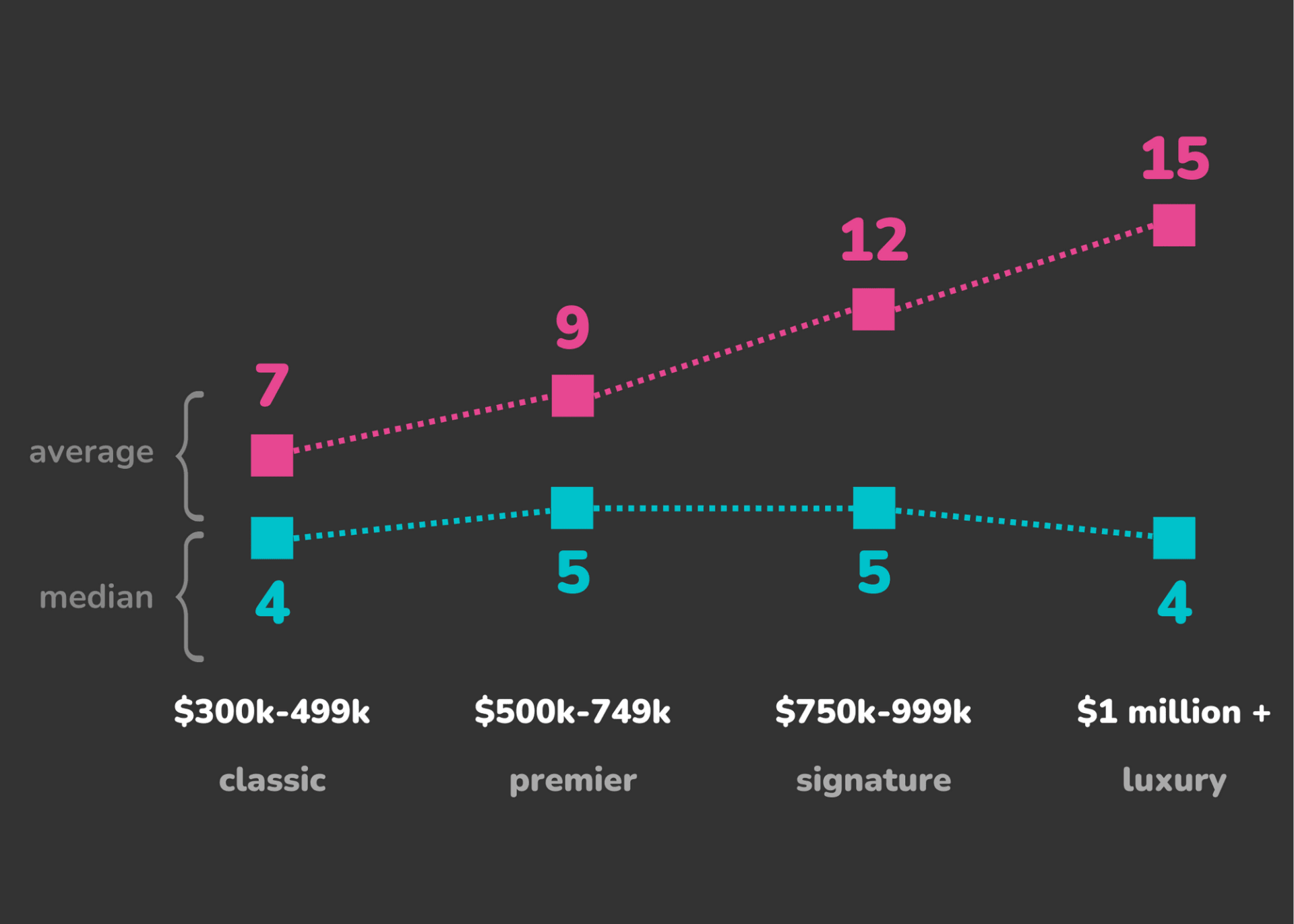

Days on Market by Segment

Days on the market inched up again in all segments and are up 1 day to 10 days over last month, a trend expected to continue with increased supply.

-

11,369 TOTAL HOMES AVAILABLE

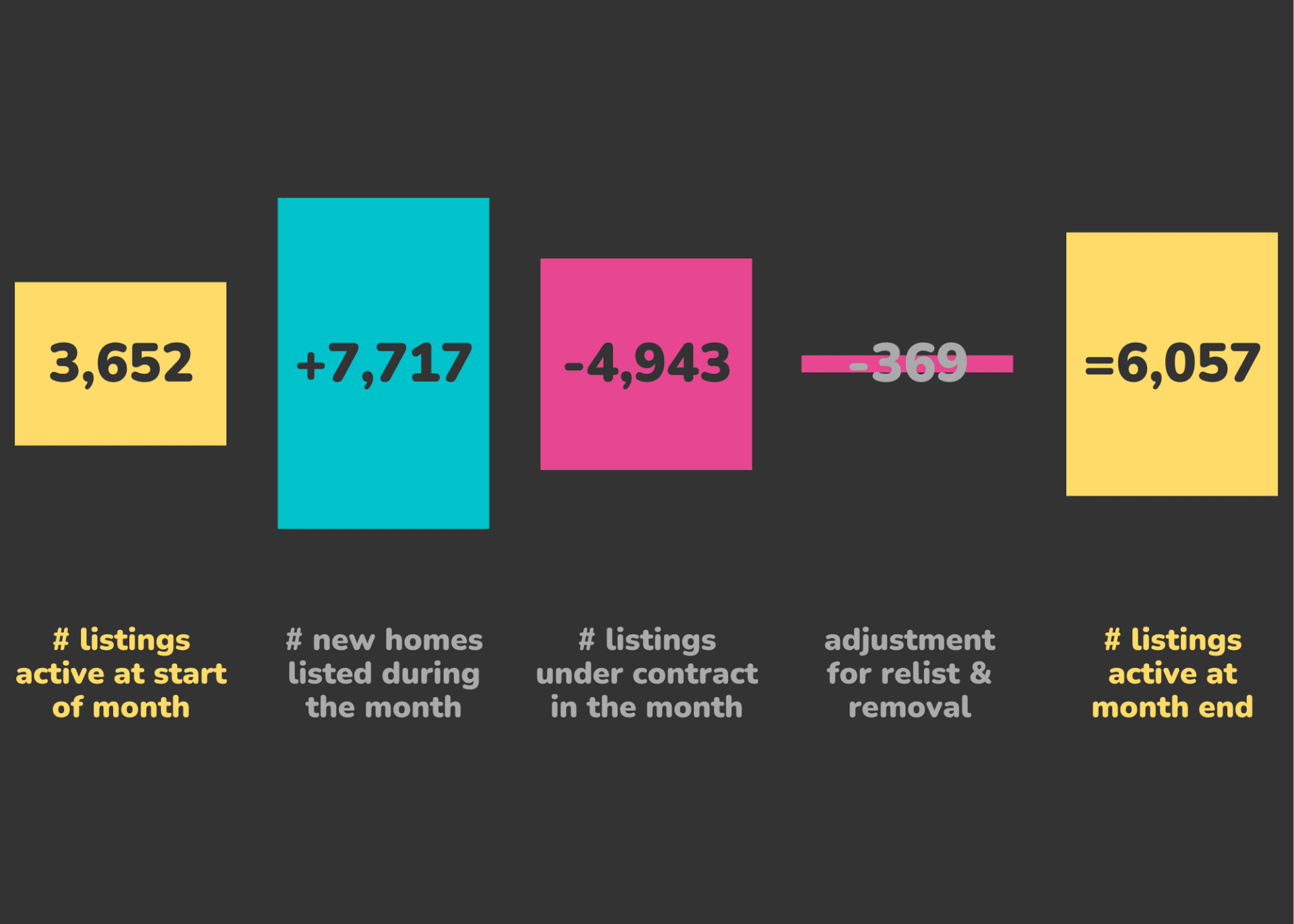

Inventory Movement

Less than half of available homes went under contract in June, pushing inventory supply above 1 month for the first time in 2 years.

Data source: DMAR Real Estate Market Trends Report

The Denver Metro Area encompasses 11 counties: Adams, Arapahoe, Boulder, Broomfield, Clear Creek, Denver, Douglas, Elbert, Gilpin, Jefferson, and Park.